The settlement for cervical stenosis from a car accident varies widely based on medical costs, lost wages, pain & suffering, and the at-fault driver’s insurance policy limits. Most cases settle between $50,000 and $500,000, but severe cases with surgery or paralysis can reach over $1 million.

If you suffered cervical stenosis from a car accident, you’re probably wondering:

How much is my case worth?

The truth is, settlement amounts depend on several factors—your medical expenses, lost wages, long-term care needs, and the at-fault driver’s insurance policy limits.

Here we’ll break down:

✅ What determines your settlement value

✅ How insurance and lawsuits pay for damages

✅ How attorney fees work (and how to negotiate them)

✅ What to do if the at-fault driver’s insurance is too low

Let’s dive into everything you need to know before negotiating your settlement.

What Factors Determine Your Cervical Stenosis Settlement?

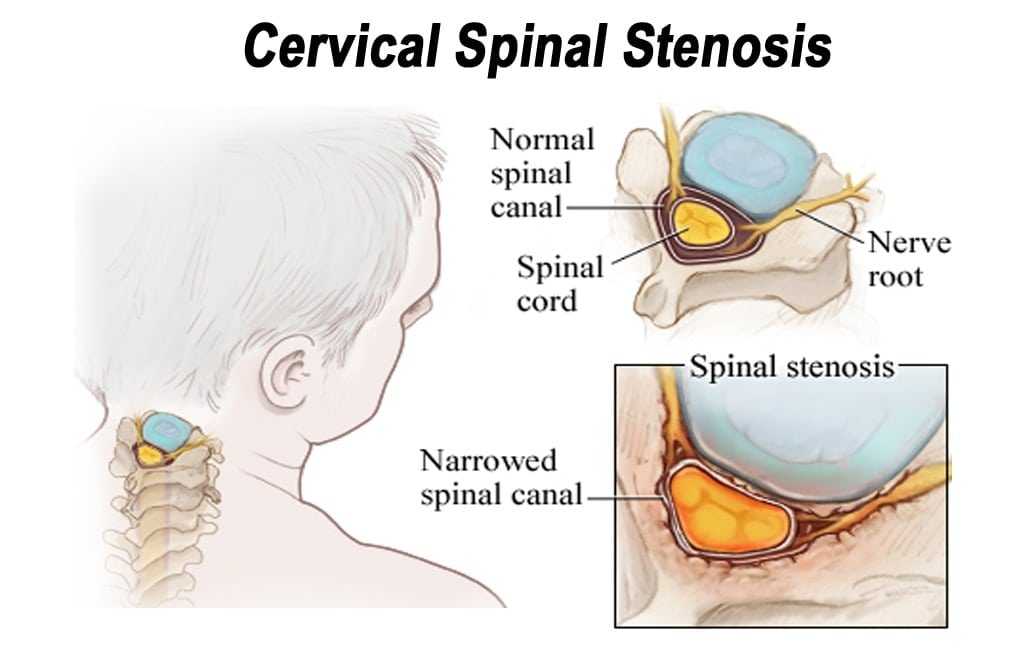

Photo Source -> Hajim School of Engineering & Applied Sciences – University of Rochester

If you’re pursuing a cervical stenosis settlement after a car accident, you should know the factors that impact your payout. The value of your settlement depends on multiple elements, including medical costs, lost wages, pain and suffering, and insurance policy limits.

Medical Expenses: The Biggest Factor

Medical expenses form the foundation of any settlement. The more severe your condition and the more intensive your treatment, the higher your settlement value.

- Immediate medical costs: ER visits, diagnostic tests (MRI, X-rays), and specialist consultations

- Ongoing treatment expenses: Physical therapy, pain management (steroid injections), and spinal surgery

- Long-term care needs: Home modifications, medical equipment, and in-home caregivers

- Future medical costs: If your spinal stenosis worsens over time, you may need future surgeries like a spinal fusion

Insurance companies often dispute future medical costs.

Proper documentation from your doctor can help justify the need for long-term care.

Helpful Resource -> Who Pays Medical Bills After A Florida Car Accident

Lost Wages & Reduced Earning Capacity

If your cervical stenosis prevents you from working, your settlement will include:

- Past lost wages – Income lost while recovering from the accident

- Future lost earnings – If your condition impacts your ability to work long-term

- Career impact – Younger victims or those with physically demanding jobs (e.g., construction, nursing) may receive higher compensation

If your earning capacity is permanently reduced, hiring an economic expert can help calculate future income losses to increase your payout.

Pain & Suffering Compensation

Unlike medical expenses and lost wages (which have clear dollar amounts), pain and suffering damages are subjective. Factors that increase non-economic damages include:

- Chronic pain that impacts daily life

- Limited mobility or reduced quality of life

- Depression, anxiety, or emotional distress from the injury

Pain and suffering damages increase significantly if the injury leads to permanent impairment or mobility loss.

The At-Fault Driver’s Insurance Policy Limits

What happens if the at-fault driver’s insurance policy is too low to cover your damages?

Here’s how it works:

- If their policy limit is $50,000, but your case is worth $150,000, their insurer only pays the policy max

- You may need to pursue additional compensation

Options if the at-fault driver’s insurance is too low:

- File a claim against your own Underinsured Motorist Coverage (UIM) – If you have UIM, it can cover the remaining damages

- Negotiate medical bills down – Some attorneys negotiate with medical providers to reduce outstanding costs

- Sue the at-fault driver directly – But this only works if they have personal assets

Many people don’t realize they have UIM coverage on their own policy. Check with your insurance company to see if you’re covered.

Where Does the Settlement Money Come From?

Many accident victims don’t know where settlement funds come from. The money doesn’t come from one place, but rather a combination of insurance policies and legal actions.

Personal Injury Protection (PIP) Insurance – First $10,000

In no-fault states, PIP insurance covers your initial medical bills and (sometimes) lost wages, regardless of who caused the accident.

- PIP typically covers up to $10,000

- Lost wages may or may not be included – Check your policy

- If medical bills exceed PIP limits, you’ll need to file a claim against the at-fault driver’s insurance

In Florida, you must seek medical treatment within 14 days of the accident to qualify for PIP benefits ➡️Florida 14-Day Accident Law | What You Need To Know

At-Fault Driver’s Liability Insurance

This is the primary source of settlement money in most cases. The at-fault driver’s insurance should cover:

✅ Medical expenses

✅ Lost wages

✅ Pain & suffering (if the state allows it)

However, their policy only pays up to the coverage limit. If your damages exceed their limits, you may need to explore additional legal options.

Uninsured/Underinsured Motorist Coverage (UIM) – A Backup Plan

If the at-fault driver doesn’t have enough insurance, you may be able to recover damages from your own UIM policy (if you have one).

- UIM kicks in when the at-fault driver’s coverage is too low

- Many drivers don’t realize they have UIM – Check your policy

- Some states require insurers to offer UIM, so you may have coverage without knowing it

Insurance companies may fight UIM claims, even from their own policyholders. An attorney can help push for a fair payout.

Lawsuits: When Do You Need to Sue?

Most cervical stenosis cases settle out of court, but a lawsuit may be necessary if:

✅ The insurer lowballs your settlement – Some insurers initially offer less than half of what a case is worth

✅ Your damages exceed insurance limits – If the at-fault driver is underinsured, you may need to file a lawsuit to recover the full amount

✅ You have a severe, permanent disability – Cases involving long-term impairment often require litigation to secure fair compensation

Most lawsuits don’t go to trial – They often result in a higher settlement offer before trial begins.

People Worrying About Losing Too Much to Fees?

One of the biggest concerns accident victims have is how much of their cervical stenosis settlement will go to attorney fees. Most people think they’ll lose a big portion of their payout, but knowing how legal fees really work could mean more money stays in your pocket.

Standard Contingency Fee: 33%-40%

- Personal injury attorneys typically work on a contingency fee basis, meaning they only get paid if you win.

- The standard fee is 33% if the case settles before filing a lawsuit and 40% if it goes to trial.

You CAN Negotiate Legal Fees

Many accident victims don’t realize that attorney fees are negotiable:

✅ Some lawyers agree to 25% if a case settles quickly without a lawsuit.

✅ If medical bills are exceptionally high, some attorneys reduce their fees to help clients take home more money.

✅ Many personal injury lawyers offer free consultations, so you can compare different firms and their fee structures.

A good attorney can maximize your settlement, even after fees, by negotiating with insurance companies and medical providers to increase your net payout.

How Lawyers Can Help You Keep More of Your Settlement

A lawyer doesn’t just take a cut—they also work to increase the amount you receive:

✔ Negotiating a higher settlement: Insurers often offer lowball settlements to unrepresented claimants.

✔ Reducing medical bills: Lawyers can negotiate bill reductions with hospitals and doctors, so you pay less out of your settlement.

✔ Protecting you from bad deals: Some insurance adjusters push quick, low offers—a lawyer ensures you don’t settle for less than you deserve.

Many attorneys front the costs of litigation (filing fees, expert witnesses, medical records) and only get reimbursed if you win—reducing your financial risk.

Do you Hate Waiting? Understand How Long It Will Take to Settle

Another concern may be how long it will take to receive settlement money. Unfortunately, there’s no one-size-fits-all answer—it depends on the complexity of your case, your injuries, and whether the insurance company cooperates.

Settlement Timelines Based on Case Complexity

| Case Type | Estimated Time to Settle |

| Simple cases (soft tissue injuries, no surgery) | 3-6 months |

| Moderate cases (herniated disc, steroid injections, physical therapy) | 6-12 months |

| Severe cases (spinal surgery, permanent impairment) | 1-2 years |

| Cases requiring a lawsuit/trial | 2+ years |

If an insurance company refuses to pay fair compensation, the case can drag out for years—but many settle before trial when insurers realize you’re serious.

Quick Settlements (3-6 months)

- Clear liability (e.g., rear-end collisions)

- Injuries that fully heal with treatment

- Insurance company cooperates

Moderate Delays (6-12 months)

- Disputes over medical costs and lost wages

- The need for ongoing treatment (e.g., physical therapy, pain management)

- Negotiations with the insurance company

Long Delays (1-2 years or more)

- Severe injuries requiring surgery or long-term treatment

- Disputes over liability (insurance company argues you were partially at fault)

- Lawsuit required (if the insurance company refuses a fair offer)

Can You Speed Up the Settlement Process?

Yes! Here’s how:

✅ Seek medical care immediately – Delays in treatment give insurers an excuse to question your claim.

✅ Document everything – Keep records of medical bills, lost wages, and daily pain levels.

✅ Work with an experienced attorney – They know how to push insurers to settle faster.

Don’t rush into a lowball settlement—it may not cover future medical expenses or lost wages if your condition worsens.

Maximizing Your Settlement: Do’s & Don’ts

The right steps can significantly increase your cervical stenosis settlement payout, while some mistakes can hurt your claim. Follow these best practices to ensure you receive the maximum compensation possible.

Get a Spinal Aesthete Diagnosis

- A general doctor’s note isn’t enough—insurers take spinal specialists (orthopedic surgeons, neurosurgeons) more seriously.

- The more detailed the medical report, the harder it is for insurers to dispute your injury.

Document Every Expense Related to Your Injury

- Keep records of medical bills, prescriptions, lost wages, travel costs for treatment, and home modifications.

- The more documentation you provide, the stronger your negotiation leverage.

Get Multiple Settlement Offers Before Agreeing

- Insurance companies lowball first offers, assuming victims will accept quickly.

- Comparing multiple offers ensures you get the best deal.

- If an insurer refuses to negotiate fairly, filing a lawsuit may pressure them into offering a higher payout.

Mistakes That Reduce Your Payout

Accept the First Lowball Insurance Offer

- The first offer is rarely fair—it’s often less than half of what your case is worth.

- Once you accept a settlement, you can’t go back and ask for more.

Post About Your Case on Social Media

- Insurance adjusters monitor social media to find reasons to deny or reduce claims.

- Even innocent posts (e.g., “Feeling better today”) can be twisted to minimize your injuries.

Skip or Delay Medical Treatment

- Gaps in treatment make insurers question whether your injury is severe.

- Consistent medical records strengthen your claim and ensure you receive full compensation.

Insurers look for any reason to reduce payouts. A well-documented case with no gaps in treatment is much harder to dispute.

What If Your Case Isn’t Worth a Lot?

Not every cervical stenosis settlement reaches six or seven figures. Many victims worry that their case isn’t worth enough to justify hiring a lawyer or negotiating a higher payout. However, even small settlements should still cover the main costs.

Even if your case isn’t high-value, these strategies can help you take home more money:

✅ Negotiate medical bills down – Some attorneys work with hospitals and doctors to lower what you owe.

✅ Ensure all expenses are included – Medical bills, lost wages, and pain & suffering should all be factored into your settlement.

✅ Avoid quick lowball offers – Insurers often underpay smaller cases, assuming victims will accept fast cash without negotiating.

Even a $10,000 settlement should cover medical costs, lost wages, and some pain & suffering. Don’t settle for less than you deserve.

When to Settle vs. When to Fight

Deciding whether to accept a settlement or go to court is one of the biggest choices you’ll face. Here’s how to know when to settle and when to fight for more.

When to Settle

- The offer fully covers medical bills, lost wages, and future expenses.

- You want to avoid the stress of a drawn-out legal battle.

- The at-fault driver has limited insurance coverage, making a higher payout unlikely.

When to Consider Suing

- The insurance company lowballs your claim, offering far less than your damages.

- Your injuries are severe, require surgery, or cause long-term disability.

- Your pain & suffering are significant, and you believe you deserve more than the initial offer.

Most lawsuits never go to trial—filing a claim often pressures insurers to increase their settlement offers.

Take the First Step Toward Justice

If you’ve been injured in a car accident, don’t wait to seek legal help. Call Applebaum Accident Group today, and we’ll connect you with the right attorney to fight for your rights.

📞 855-225-5728 | Request Your Free Consultation Now

With Applebaum Accident Group, you get support, expertise, and access to Florida’s best attorneys – without the stress. Let us help you find the legal representation you deserve.