If you’re hit by a driver without insurance in Florida, your Personal Injury Protection (PIP) covers initial medical costs. If damages exceed that, you may rely on Uninsured Motorist (UM) coverage or sue the at-fault driver, but recovery depends on their ability to pay.

You did everything right. You bought insurance, followed the rules, drove safely, and then someone without insurance rear-ended you.

They’re at fault, but they don’t have coverage. You’re hurt, your car’s a mess, and the bills are piling up. What now?

Unfortunately, this scenario isn’t rare. Florida has one of the highest rates of uninsured drivers in the country. That means many accident victims find themselves stuck, wondering who’s going to pay for their medical bills, lost wages, and vehicle repairs.

Will your insurance help? Can you sue the driver? How much will a lawyer take if you win a settlement? And what happens if the driver can’t pay a dime?

This article breaks down everything you need to know after a car accident with an uninsured driver in Florida. You’ll learn how PIP coverage works, when UM/UIM coverage can help, how lawsuits really play out, and what to do if your own insurer drags its feet. We’ll walk you through real questions and frustrations people face, so you’re not just prepared, you’re protected.

Who Pays if the Other Driver Has No Insurance in Florida?

Florida follows a no-fault system, meaning your own car insurance, specifically, your Personal Injury Protection (PIP), covers medical expenses and lost wages after a crash, regardless of who caused it.

This applies even if the at-fault driver has no insurance at all.

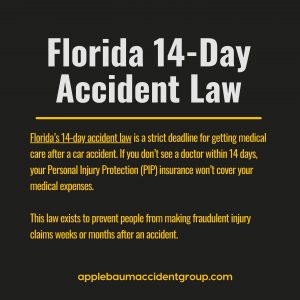

Your PIP coverage will pay 80% of your medical bills and 60% of your lost income, up to a combined maximum of $10,000. Florida law requires that you seek medical treatment within 14 days of the accident. Miss that window, and you may forfeit your PIP benefits entirely under F.S. 627.736.

So what happens when your costs exceed $10,000? That’s where things get complicated, and often expensive. If you need ongoing treatment, surgery, or have significant pain and suffering, PIP likely won’t cover it. And if the driver who hit you doesn’t have liability insurance, or assets, you may be left scrambling for alternatives.

What If My PIP Doesn’t Cover Everything?

This is where Uninsured Motorist (UM) coverage becomes a financial lifesaver, if you have it.

UM coverage (or Underinsured Motorist, UIM, for cases where the at-fault driver has some insurance, just not enough) can cover damages beyond PIP, including medical bills, pain and suffering, future care, and long-term lost wages. It essentially steps in to act like the insurance the other driver should have carried.

Many Florida drivers unknowingly decline UM coverage. Insurers in Florida are only required to offer it, you have to opt in. Many people waive it at signup without realizing what they’re giving up. And after the crash, they find out too late.

Even if you have health insurance, it doesn’t always solve the problem. Some plans require reimbursement if you receive a settlement, which means the money you thought you could keep ends up going right back to your insurer.

That kind of stress is all too real. If you’re stuck without UM or enough PIP, you might be considering legal action, but that’s a tough road if the at-fault driver has no money to begin with.

What If I Don’t Have UM Coverage Either?

If you don’t have UM coverage and your expenses exceed PIP, your remaining option may be to sue the uninsured driver directly.

Under Florida law, you can file a personal injury lawsuit against the negligent driver, especially if your injuries meet the threshold to exit the no-fault system, such as permanent disfigurement or disability.

Many uninsured drivers are “judgment-proof.” That means they don’t have enough income, assets, or property for you to collect anything meaningful, even if you win. In some cases, a court can garnish wages, place liens on property, or even levy bank accounts. But if the other driver has minimal or exempt assets, there’s often nothing to recover.

The Driver Gave Fake Insurance or Fled the Scene?

Unfortunately, some drivers don’t just lack insurance, they lie about it or disappear altogether. Fake insurance cards and hit-and-run accidents are all too common in Florida, especially among uninsured or undocumented drivers trying to avoid legal consequences.

If the driver flees or provides false insurance information, your case may qualify as an uninsured motorist claim, but it hinges on how you document the incident. This is where a police report becomes absolutely critical.

Without it, your insurer may reject the claim or argue that the driver wasn’t truly uninsured.

UM coverage can still apply in these scenarios, but only if you act fast. Call 911 immediately after the accident, even if the damage seems minor. Insurers may require proof that you made a timely effort to report the hit-and-run and verify the other party’s uninsured status.

Delays can destroy your claim. Victims who wait to seek treatment or contact police often find themselves out of options when insurers push back.

You Still Can Sue the Uninsured Driver

Yes, you can sue an uninsured driver in Florida, but the right to sue depends on the severity of your injuries. Under Florida’s no-fault law, you can’t pursue the at-fault party directly unless your injuries are considered “serious.” That typically means:

- Permanent injury or disability

- Significant disfigurement or scarring

- Loss of bodily function

If your injuries qualify, you can step outside the no-fault system and file a personal injury lawsuit for full damages, including pain, suffering, and future medical care.

Keep in mind, though, that Florida law gives you four years from the date of the accident to take legal action (F.S. 95.11). But waiting that long rarely helps your case, especially when evidence degrades and memories fade.

And even if you win? There are three likely outcomes:

- Settlement: You reach an agreement, possibly through negotiation or mediation.

- Default judgment: The defendant doesn’t respond, and the court rules in your favor.

- Nothing recovered: The driver has no assets or income to collect from.

When You Are Partially at Fault

Florida follows a comparative negligence rule, which means more than one person can share blame for an accident, and your compensation is reduced by your percentage of fault.

Let’s say the uninsured driver ran a red light, but you were texting while driving. If the court finds you 20% responsible and awards $100,000 in damages, you’d receive $80,000.

“What if I was texting but they ran a red light and had no insurance?”

In that case, you may still recover money, but less than if you were completely blameless.

This becomes especially relevant in UM claims, where your own insurer may argue you were partly at fault to limit the payout. Even in a lawsuit, the defense will likely use comparative negligence to reduce liability. That’s why clear evidence, dashcam footage, witness statements, police reports, is your best protection.

The Driver Has Nothing, Now What?

If the uninsured driver has no car insurance and no UM coverage applies, you’re likely looking at a lawsuit. But winning in court doesn’t guarantee payment. That’s where collection strategies come in, though they’re not easy or fast.

Here are a few legal tools that may help:

- Wage garnishment: A portion of the driver’s paycheck is diverted to you.

- Liens on non-homestead property: If they sell assets like land or a second car, you get paid first.

- Bank levies: A court can order the seizure of funds in their bank account.

- Payment plans: Some judgments are satisfied over time in small monthly installments.

Harsh reality. Many uninsured drivers file for bankruptcy.

If they file under Chapter 7, your judgment may be wiped out, especially if the court doesn’t find gross negligence or intentional misconduct. That means even after all your effort, you might receive nothing.

That’s why recovery planning needs to happen before you file a lawsuit, not after.

What Else Could Help Pay My Bills?

If you’re coming up short on PIP and don’t have UM, you may still have options buried in your own insurance policy:

- Medical Payments (MedPay): Covers out-of-pocket expenses not paid by PIP.

- Collision coverage: Pays to repair your car, even if the other driver is uninsured.

- Health insurance: Can step in, but may demand reimbursement if you win a lawsuit or UM claim.

Some victims also turn to crowdfunding platforms like GoFundMe to cover rent, medical bills, and recovery costs. These campaigns don’t interfere with your case, but they do raise legal questions if you later receive a settlement.

Protect Yourself Now, Before It Happens

If you’re reading this before a crash, not after, this is your moment to prepare. Three things to review today:

- UM/UIM coverage: Add it or increase your limits. It’s your last line of defense

- (2) Medical Payments (MedPay): This can help fill the gaps in PIP, especially with co-pays and deductibles

- (3) Collision coverage: Covers vehicle damage if the other driver has no insurance or flees the scene.

Don’t wait until you’re dealing with the aftermath of a car accident to realize your policy falls short. A few proactive adjustments can be the difference between full recovery and financial disaster.

Can I Sue My Own Insurance Company?

If you have Uninsured Motorist (UM) coverage and your insurer denies or undervalues your claim, you may have grounds to file a bad faith lawsuit.

Under Florida law (F.S. 624.155), insurers are required to act fairly, promptly, and in your best interest. When they delay payment, offer unreasonably low settlements, or deny valid claims without explanation, they may be liable for additional damages.

UM claims are especially vulnerable to bad faith tactics. Why? Because unlike liability claims where two separate parties are involved, here you’re going up against your own insurance company, a company you paid to protect you.

It’s also common for UM policies to include mandatory arbitration clauses. This means you might not get a jury trial, and instead must resolve the claim in private arbitration, where insurers often have a home-field advantage.

Delays. Lowball offers. Endless requests for documentation. These are real issues policyholders face, even with valid claims. If you’re dealing with this kind of runaround, legal action may be the only way forward.

If You Are a Tourist or Visiting from Out of State

Florida’s no-fault system applies to everyone injured in a car accident on Florida roads, including out-of-state visitors.

That means if you’re visiting from Georgia, New York, or even Canada, your access to compensation is governed in part by Florida’s PIP laws, not just your home state’s policy.

This causes massive confusion. Some non-residents assume they can sue the at-fault driver immediately, only to find out that Florida law limits lawsuits unless their injuries qualify as “serious.”

If you’re from a tort state, your insurer may step in differently than expected. For international tourists or those in rental cars, things get even messier. Rental agreements vary, and international travelers often aren’t clear on whether their travel insurance includes UM or medical payments.

If you’re injured in Florida and don’t know where to turn, it’s critical to speak with a professional who understands both Florida law and cross-jurisdictional claims. The right legal team can make sure you don’t miss benefits you’re entitled to.

Take the First Step Toward Justice

Applebaum Accident Group connects you with trusted attorneys who understand what your case is worth, and how to make sure you don’t settle for less.

📞 855-225-5728 | Request Your Free Consultation Now

With Applebaum Accident Group, you gain access to Florida’s top legal and medical networks, without the stress or confusion. We help you move forward with confidence, clarity, and the support you need.